Newsletter

Winter 2016

Making Tax Digital

Starting in April 2018, the government intends to implement major plans to modernise the tax administration system by introducing digital services for tax. This Briefing looks at the key changes proposed in HMRC consultations issued in August 2016.

There are three main strands to these proposals, as follows:

- personalised digital tax accounts for individuals and for businesses

- quarterly digital reporting of income and expenditure by businesses, self-employed people and landlords

- options for paying tax.

Digital tax accounts

Digital tax accounts for individuals have already been created by HMRC. These are called Personal Tax Accounts. These accounts have been linked to HMRC internal systems so that they will be pre-populated with income and tax details that HMRC already hold. This includes employment income, PAYE and NIC and any state retirement pension. From April 2018, it is intended that interest paid by banks and building societies will be included in digital tax accounts. In order for this to happen, banks and building societies will be required to provide information to HMRC earlier, and more frequently, than currently. Taxpayers will also be able to report any additional sources of income through their digital tax accounts in 2018.

HMRC expect that with pre-populated information and taxpayers able to add in other sources of income, the digital tax account will mean that a significant number of taxpayers, with relatively straightforward tax affairs, will not need to complete a tax return.

Digital tax accounts are also being established for businesses and these will show an overview of the income tax or corporation tax, VAT and NIC details of the business. In order to show details of the income subject to income tax or corporation tax, details of the business's income and expenses will be provided by new quarterly tax updates.

Quarterly updates

By 2020, most businesses, self-employed people and landlords will be required to keep track of their tax affairs digitally and update HMRC at least quarterly through their digital tax account. These changes will be phased in from 2018 with the start date depending on a business's accounting period (see the example later in this Briefing). These measures will not apply to unincorporated businesses or landlords where their turnover or gross income from property is under £10,000. Some businesses and landlords with income above £10,000 will also benefit from a deferral of the new rules by one year. The upper threshold and eligibility for this deferral have not been detailed in the consultations. Charities and Community Amateur Sports Clubs are also likely to be exempted from these new rules.

To meet these quarterly reporting requirements, taxpayers will be expected to use software or apps which record day-to-day transactions, categorise them into different types of income or expenses and then feed the summary data directly into HMRC systems. HMRC has no plans to offer free software but expects developers to provide free software for businesses with the most straightforward affairs.

Example

|

|

Craig is a builder and is using a smartphone app to digitally record his business transactions. Using the app he takes a photo of receipts he receives from his suppliers and the software prompts him to confirm that the cost is business related and, if so, what expense category the purchase relates to. After a short time of keeping his records in this way the software automatically allocates expenses depending on his most used categories.

During the year Craig buys a van for the business. When entering the details into his app, the software creates a message which advises Craig of capital allowances which are available on the purchase of vans. This message has a link to further details. On entering the cost of the van, the software calculates the capital allowances due and updates Craig's tax position.

|

The periodic updates of data to HMRC will be made quarterly but could be done more frequently if a business or landlord chooses. When an update is due, businesses and landlords will have one month to compile the information and declare that the period's data is complete to the best of their knowledge.

In order to help the self-employed and landlords meet these additional reporting requirements, HMRC are consulting on a range of options including:

- the extension of cash basis accounting to more businesses and allowing unincorporated property businesses to use the cash basis

- the reduction in the number of accounting adjustments required to arrive at a taxable profit or loss.

Please let us know if you would like further details of these changes.

What about partnerships?

The consultations propose that a partnership, through a nominated partner, would fulfil the obligations of record keeping on behalf of the partners. The partnership's updates would then feed directly into each partner's digital tax account as pre-populated income based on the profit allocation of the partnership. Therefore individual partners would not have to maintain their own digital records. A similar approach would be taken for jointly held property which is let out.

The 'End of Year' return

Throughout the year, businesses will have provided HMRC updates of their business income and expenditure. After the end of the year, having made any adjustments to arrive at their taxable profit or loss, businesses will make an 'End of Year' declaration that everything is correct and complete. This declaration will be made within nine months of the end of a period of account (normally a period consisting of four consecutive quarterly returns).

Example - start dates and timings for quarterly accounting

|

|

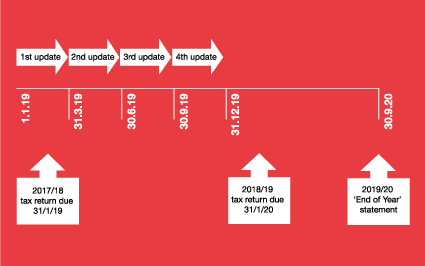

Jamie has a plumbing business and he prepares accounts running up to 31 December. Jamie has decided to do quarterly updates rather than more frequent ones. He will begin his first update cycle on the first day after the first accounting date that follows 5 April 2018. The first accounting date is therefore 31 December 2018 and he will start his updates on 1 January 2019.

Consequently the first cycle of quarterly updates will be as set out in the diagram below. Jamie would still need to make self assessment tax returns for 2017/18 and 2018/19. For 2019/20 there would be no need for a self assessment tax return but Jamie would need to make an end of year declaration by 30 September 2020.

|

|

Tax payment changes

Businesses, self-employed people and landlords, who are keeping their records digitally, will be able to adopt pay-as-you-go tax payments on a voluntary basis. There are however no plans to change the dates by which income tax is due.

For employees, HMRC has already started using real-time PAYE data to reduce under and overpayments by changing tax codes in-year. They are proposing to extend this principle through individuals' digital tax accounts to include common income types in the in-year tax calculations. In principle, tax arising on additional income which is small or regular will be collected through PAYE tax code changes. On larger amounts of income, individuals will be advised through their digital tax accounts how much tax will become due after the end of the tax year and will be given options on how and when to pay what is owed.

Better use of information

Starting from April 2017, HMRC will start to use PAYE information during the tax year to calculate whether the right tax is being paid and to notify taxpayers through their digital tax accounts when this is not the case. This will particularly benefit employees who have seasonal work or multiple PAYE income sources. The next step towards using third party information is to include common income types in the in-year calculations of tax on a more frequent basis, starting with bank and building society interest from April 2018. The objective is to prevent tax owed on other modest income sources from accumulating during the year by collecting the tax due through PAYE.

These changes will mean an increase in tax codes being issued to employers but HMRC believe that as these should automatically be adjusted through computerised payroll systems there should not be any increased demands on employers' time. HMRC do recognise, however, that more frequent changes in PAYE could create additional queries for employers from their employees. To help with this, HMRC are proposing to give full details of any changes in employees' digital tax accounts so they should be able to fully understand the amendments and therefore not need to query further with their employers.

Example

|

|

Claire works in a printing business as a marketing manager, she is also employed by her local gym as a gym instructor. The amount of her work in the gym can vary because of fluctuating demand for her classes. In prior years she received multiple tax code changes during the year as sometimes she moved into a higher tax band. In addition she often had an under or over-payment of tax at the end of the year.

Having set up a digital tax account, Claire receives a text message to alert her to a change in her tax position. Logging on to her account, Claire can see that because it is summer and her classes have reduced she is no longer liable to pay tax at a higher rate. This is explained through her digital account and she does not need to contact HMRC for any extra information. The account also confirms that her employer has already been notified of this change.

|

Timeline - key dates

|

November 2016

|

Consultations on Making Tax Digital closed

|

Accounting periods starting after:

|

|

April 2018

|

Quarterly updates for unincorporated businesses and landlords

|

|

April 2019

|

VAT comes within Making Tax Digital

|

|

April 2020

|

Quarterly updates for companies

|

How we can help you

At the moment, you do not have to do anything in respect of these developments. If you do want to access your digital tax account you may need to verify your identity. You can find details at: www.gov.uk/personal-tax-account. If we are your tax agents, we cannot access the account on your behalf.

If you would like to know more about the proposed changes under Making Tax Digital and what they could mean for your business, please do not hesitate to get in touch with us.